Shortly after the Capital One-Discover deal received sign-off, Columbia, Eastern and Cadence Bank all announced deals. So did a host of smaller institutions.

By: Dan Ennis• Published April 30, 2025

For months, the Capital One-Discover deal had been spotlighted as the bellwether for how bank mergers and acquisitions could go under a second Trump administration.

Not just the will-they-or-won’t-they (as in, would regulators sign off on the combination?), but how long will transactions sit in evaluation? Which potential stumbling blocks would be eased or de-emphasized?

Since the $35.3 billion Capital One deal received green lights from the Federal Reserve and Office of the Comptroller of the Currency, it’s fair to say bank M&A is off to the races.

Perhaps the first clue that the bank-mashup floodgates had opened came when Columbia Banking System said it would buy Pacific Premier Bank in an all-stock $2 billion deal that would cement the Pacific Northwest juggernaut deeper into Southern California.

But the dominoes continued. The next day, Boston-based Eastern Bank announced it would merge with in-state competitor HarborOne in a $490 million cash-and-stock deal. A day later, Cadence Bank said it would buy Industry Bancshares, the beleaguered holding company that owns six community banks in Texas, for between $20 million and $60 million in cash.

And that’s just banks that hold $25 billion or more in assets. Smaller deals in Pennsylvania and Tennessee, for example, have followed – as has a partial-bank transaction in which St. Louis-based Enterprise Bank & Trust will acquire 10 locations in Arizona and two in Kansas from Montana-based First Interstate Bank.

That M&A is ramping up shouldn’t be a surprise. Christopher Olsen, managing partner and co-founder of investment-banking firm Olsen Palmer, told Banking Dive in March that smaller banks, in particular, have felt consolidation pressure for several years, adding that Trump’s reelection could act as “sort of the powder keg” to drive that trend.

Shorter timelines

Some of the participants, on the other hand, may be a surprise. It would be understandable if Columbia had been trigger-shy on acquisitions. Its $5.2 billion merger with Umpqua Bank, announced in October 2021, took more than 16 months to close – and did so less than two weeks before Silvergate, Signature and Silicon Valley Bank failed.

Columbia CEO Clint Stein, in a call addressing the Pacific Premier deal, pointed to a "seismic shift in the operating or rate environment" during the Umpqua integration, according to American Banker. Stein, however, characterized today’s M&A environment as more “conducive” by comparison.

The roughly $50 billion-asset Columbia said it expects the Pacific Premier deal to close in the second half of this year – meaning it estimates the transaction will await regulatory approval only half as long as the Umpqua deal did.

"There's a body of evidence that continues to build on deals getting approved quicker for banks either our size or to create banks that are our size," Stein said last week. "The other thing is that we had fairly robust pre-flight conversations with the regulators, both at the regional office level as well as in D.C."

A shorter approval timeline would no doubt appease some regulators. Federal Deposit Insurance Corp. Acting Chair Travis Hill put more timely bank merger approvals among his 15 priorities beginning on his first day leading the agency.

Since Trump regained office, the timeline for several deals has shortened. Evansville, Indiana-based Old National disclosed that it expects its $1.4 billion acquisition of Bremer Bank to close May 1. That’s likely a quicker turnaround than the more vague “mid-2025” time frame the bank gave when the transaction was announced. In any case, it would mean the tie-up would have spent barely five months in evaluation.

By comparison, Mississippi-based Renasant’s acquisition of The First Bancshares – a similar value at $1.2 billion – took eight months to approve. UMB’s $2 billion acquisition of Heartland Financial took nine.

Old National is not alone in its truncated timeline. When Busey Bank announced in August (before Trump’s reelection) that it planned to buy CrossFirst, it initially gave itself a 10-month timeline. The deal closed in six. Likewise, Atlantic Union Bank gave itself a year to close its $1.6 billion acquisition of Sandy Spring. It wrapped in just over five months.

Sometimes longer timelines can’t be helped. Columbia’s Umpqua deal, for example, saw an 11-month Justice Department investigation. The Capital One-Discover deal awaited regulator approval for 14 months likely out of caution for its size and potential impact.

Mergers and acquisitions still likely will face pitfalls. U.S. bank stocks saw their worst quarterly loss since in two years over 2025’s first 90 days. And if bank valuations indeed “grease the skids” of M&A, as Olsen put it, deals with a cash component may prove an easier sell.

Article top image credit: Mario Tama via Getty Images

Frost CFO: ‘We are that stable bank in Texas’

The San Antonio lender has hung its hat on long-term organic growth. “We get to bring in customers that chose us, not that we bought,” said Dan Geddes, a 28-year Frost veteran.

By: Caitlin Mullen• Published July 9, 2025

When Dan Geddes interviewed at Frost Bank nearly three decades ago, he met with people who’d been at the bank for 28 years – a stark contrast to other banks where he interviewed, whose employees had far shorter tenures.

Geddes himself has now been at the San Antonio-based lender for 28 years and, at the beginning of the year, filled the chief financial officer seat vacated by Jerry Salinas, who retired at the end of 2024.

“I remember thinking, ‘I've got to find out why people stay here so long,’ and now I'm that person that's been here forever,” said Geddes, who comes to the CFO role by way of the commercial bank, rather than accounting or finance. “It just doesn't happen very much anymore in most industries and most companies.”

To Geddes, it speaks to the culture of the 157-year-old institution, and preserving that culture as the bank has expanded across the state is a top priority, he said during a recent interview.

Dan Geddes

Permission granted by Frost

“We are that stable bank in Texas,” he said.

Amid recent deadly flash flooding, parts of Texas undoubtedly are seeking stability.

To that end, the lender’s Hill Country branches will direct a $500,000 grant from the Frost Bank Charitable Foundation to the Community Foundation of the Texas Hill Country’s Kerr County Flood Relief Fund and other local flood-relief efforts, the bank said.

Communities in the county, including Kerrville, Hunt, Ingram, are among the hardest hit after torrential downpours July 3 sent the Guadalupe River surging 22 feet in flooding that killed at least 110 people, while as many as 173 more remained missing as of July 9.

“There are so many of us at Frost who know someone who either was affected by the disaster or who is connected in some way with the affected people and communities,” Kevin Thompson, the bank’s said Hill Country market president, said in a news release. “We’re heartbroken by the devastation, and our hearts go out to the families of those who died or were injured.”

Frost is making emergency disaster loans available to borrowers, and contacting customers in affected areas to discuss ways to temporarily defer loan payments if needed. Frost has a branch in Boerne – in neighboring Kendall County, which also saw flash flooding – and is building new locations in Kerrville and Fredericksburg.

Frost’s operations were unaffected and the $52 billion-asset bank’s branches remain open, a spokesperson said.

Consistency and dependability have been key to Frost’s identity, Geddes indicated.

When other banks have taken more aggressive pricing structures during robust economic times, Frost has lost some deals, he said, “but we more than make up for it when there is uncertainty.”Prospects were much more willing to talk to Frost during tougher times, when others had backed away, Geddes said.

In pursuing organic growth, CEO Phil Green “has shown the willingness to make investments to help support long-term growth, instead of being overly focused on quarterly earnings or chasing the flavor of the month in banking,” D.A. Davidson analyst Peter Winter wrote in a recent note.

The bank is keeping its head down on its expansion strategy, and remains definitively uninterested in M&A, Geddes said.

“We get to recruit the bankers that want to be with us, not the ones that we inherited,” Geddes said. “We get to bring in customers that chose us, not that we bought and we're trying to maintain. And we get to choose the locations; we’re not stuck with the locations of the bank that we bought.”

Frost also maintains better control of its culture and avoids the distraction of systems integrations that acquisitions require, he asserted.

Although the bank may someday pursue expansion outside Texas as it inches toward $100 billion in assets, Geddes said Frost has plenty of room to grow within the state.

The bank is only scratching the surface in the state’s biggest markets, Houston and Dallas, in terms of deposits, Geddes said. In Houston, Frost has about 5% of bank branch share, but only 2.5% deposit market share; in Dallas, Frost has a 3.6% branch share and about 1% deposit market share, Geddes said. By comparison, Frost has a 10% branch share and 27% deposit market share in San Antonio and a 9% branch share and 25% market share in Corpus Christi, Geddes noted.

Frost is “planting trees, not corn,” and the expansion strategy requires patience, bank executives have said. The bank has close to 200 branches across the state. The average age of new branches in Houston is about five years, while Dallas is about two years and Austin – where the bank said in 2023 it planned to double its branch presence – is less than one. After four years, the bank generally starts reaping what’s been sown, Geddes said.

In most of Frost’s markets, money center banks have about 50% or more of the market share, he said. Frost gets about half of its new commercial relationships from those banks, seeking to compete by focusing on customer service, personal touch and the ability to talk to decision-makers.

Frost also recruits experienced talent from those big banks and smaller lenders, but is less interested in acquiring teams of bankers.

“We don’t look to bring over teams. We find that that can create little subcultures within your organization,” he said.

Article top image credit: Permission granted by Frost

BofA’s head of branches: ‘Proximity is still important to people’

Customers may or may not visit a branch, but the bank’s presence affirms its commitment to a community, and “there’s a brand value” in that, the executive said.

By: Caitlin Mullen• Published June 3, 2025

To Bank of America, it’s become clear that “you have to be proximate to your clients,” said Will Smayda, the lender’s head of financial centers.

“They may or may not visit you,” he quickly added. But the bank’s presence affirms its commitment to a community, and “there’s a brand value” with that, Smayda said.

Even as 90% of the bank’s client interactions now occur digitally, “proximity is still important to people, and I think it will be, into the future,” he said during an interview.

In May, the Charlotte, North Carolina-based lender said it planned to open 40 new branches by year’s end, and 110 additional locations between 2026 and 2027. Bank of America has invested $5 billion in new and existing locations since 2016.

Will Smayda

Permission granted by Bank of America

The bank has about 3,700 branches across some 200-plus markets. Its branch count has shrunk by about 21% over the past 10 years; in 2015, the bank had about 4,700 branches.

To get there, the bank has pursued what it calls “consolidations,” Smayda said.

“What we’ll find is two financial centers that we’ve had for decades may be supporting a neighborhood, and instead of heavily reinvesting in one or the other, we’ll close both and put up a new building,” he said.

In those new builds, the changed format features more space for conversations, and screens take the place of more static marketing.

As its branch count has fallen and digital banking has become the norm, the bank’s tally of consumer and small business customers has grown by about 47% in the past decade, and the assets those customers keep at the bank has climbed, Smayda said.

But branches still have a place, and BofA isn’t alone in its push to open more: JPMorgan Chase, PNC, Fifth Third and Huntington are among other banks pursuing meaningful branch expansion.

Bank of America sees about 600,000 clients a day in its branches, and most new customers come to the bank through branches, Smayda said.

“A majority of that new client work happens in our financial centers, so they are crucial to us,” Smayda said of branches. “We want to be there for when they make that decision, we want to make that easy for them.”

The bank had about 10 million appointments with its customers in 2024, he said. As more basic banking functions are done online and physical locations become hubs for advice and in-depth information, professional services-type appointments are replacing the old transactional mode in branches, he noted.

When asked whether he expects the branch total to continue dropping over time, Smayda said the bank will “probably, net, continue to trend down a little bit” – though any slimming won’t stem primarily from a need to cut costs.

“How many we keep, that’ll be dictated by, really, client behavior,” he said. “We’ll adapt to what our clients need from us.”

Adding to the retail footprint

The bank was open four branches in Boise in June. Idaho’s population has swelled as residents of states like California migrated during the COVID-19 pandemic, with some movers being existing Bank of America customers, Smayda said.

Boise is one of 20 markets where the bank has long had a presence, between its Merrill Lynch entity and commercial and business banking, “but we’ve not had a consumer footprint,” he said.

In a couple of years, Bank of America will do the same in Wisconsin, Louisiana and Alabama, although the bank hasn’t shared dates or locations yet, Smayda said.

In evaluating the viability of branches, Bank of America considers demographics all retailers do, he said. Is the community growing or shrinking? What businesses anchor the community? How is the community served today by the lender, if it’s a market BofA is already in – or by competitors, if it’s not? The answers to those questions determine the number of branches needed, he said.

As far as measuring success once branches have opened, Smayda said the bank takes a close look at its existing clients, including, for example, commercial clients whose employees may need consumer banking. “Do they choose to grow with us faster, because we now have a presence?” he said.

The bank aims to become a top three financial services company in each market it’s in. “In the community, how quickly can we take market share?” he said. “That is probably the single kind of unifying metric.”

In places like Boise, Dallas or Charlotte, “we have to keep up with these communities as they grow,” Smayda said. At the same time, the bank has customer bases it wants to retain and grow in existing areas, pointing to the importance of investing in legacy and newer growth markets. “You’ve got to be both,” he said.

Some new branches lack traditional banking services that have become less frequently used by customers today.

Night drops or safe deposit boxes are “not as interesting to today’s business owners or today’s clients,” Smayda said.

“We will sometimes open without them, and because it’s not a service we’ve ever offered … it’s not missed,” he said.

Today’s customers, Smayda noted, are more inclined to seek fraud protection or education.

In any case, he said, branches are “critical for the foreseeable future.”

Article top image credit: Brandon Bell / Staff via Getty Images

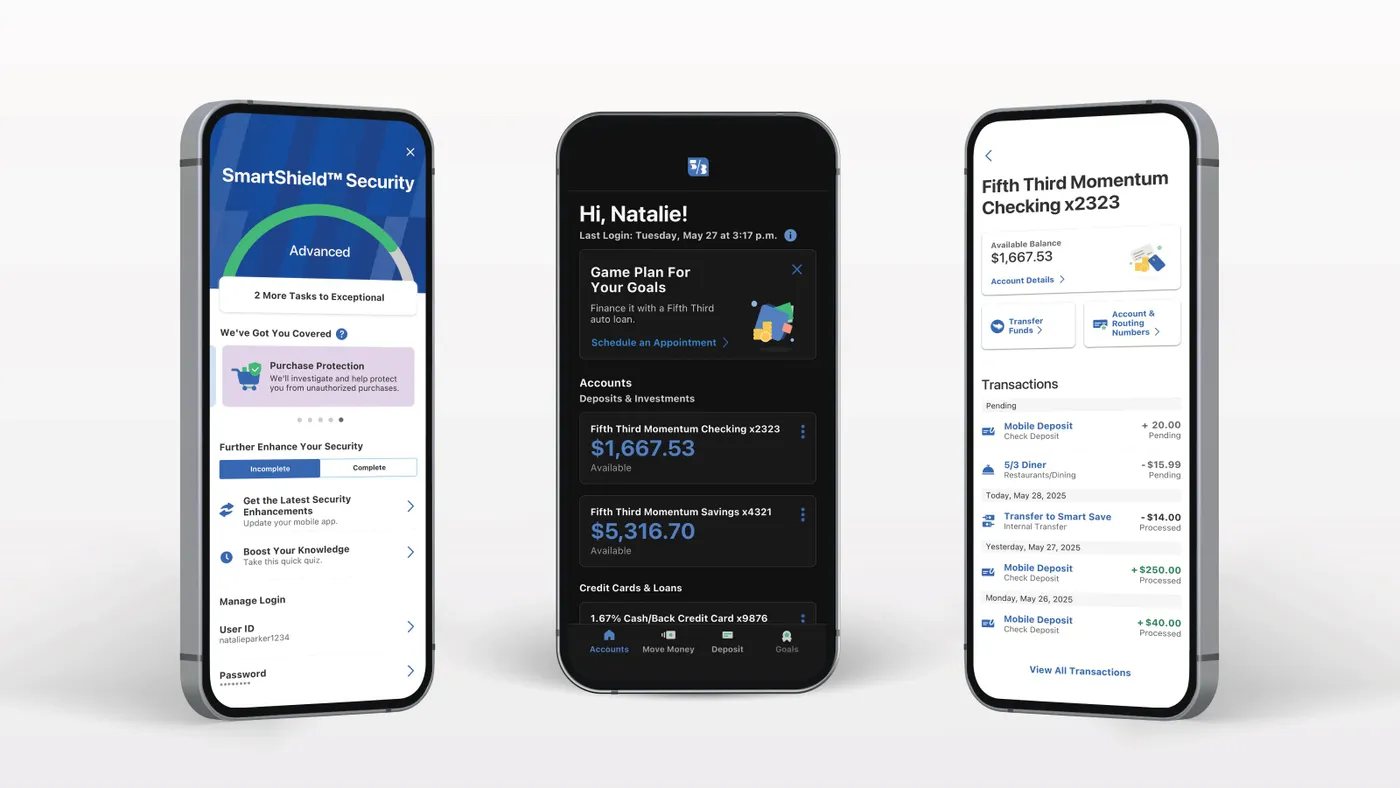

Fifth Third takes ‘intentionally unsexy’ approach to mobile app improvements

“It is more important to customers that banking works, than that banking is delightful,” said Fifth Third’s chief strategy officer and head of consumer products.

By: Caitlin Mullen• Published June 6, 2025

Ben Hoffman has no doubt Fifth Third Bank’s peers and competitors are mulling some of the same mobile app features and enhancements as the Cincinnati-based lender.

“There is more convergence in bank strategy than there is in bank execution,” said Hoffman, Fifth Third’s chief strategy officer and head of consumer products.

“It’s really about your ability to execute” at a sustained pace, he said.

For Fifth Third, that means leaning on dedicated staff, operating rhythms and experience, and systems set up to support success, he said.

Ben Hoffman

Permission granted by Fifth Third Bank

In May, Fifth Third was named best mobile banking app experience among regional banks in a J.D. Power survey. The bank’s app offers services like direct deposit switching and card controls, and features tools like SmartShield, its in-app security tool that “gamifies” digital safety. The lender continues to work on enhancements to the app, which about 2.4 million bank customers use to handle everyday banking tasks.

In Hoffman’s eyes, the $212 billion-asset bank’s approach stands out in part because of its focus on quality over quantity.

“We focus on quality where it matters, with the core theory being that, for the most part, our customers want banking to fade into the background,” he said. Rather than stuffing apps with features or equipping chatbots with an ever-growing roster of skills, “it needs to just work to support real lives.”

When Fifth Third releases a new feature in the mobile app, automated monitoring is set up to ensure the process works well; if there are defects, point people are contacted and troubleshooting begins. Product managers join release calls, no matter the hour, he noted.

It’s an “intentionally unsexy” approach, he said.

“It’s really about focusing on the things that matter to our customers and not falling in love with the thing that feels exciting and feels different,” Hoffman said. “It is more important to customers that banking works, than that banking is delightful.”

The bank’s technology and communications spending has ticked up in recent years, from $416 million in 2022, to $474 million in 2024, with increased investments in technology modernization being one of the drivers, according to Fifth Third’s annual filing. Bank executives, when reporting Q1 earnings in April, said technology investments would continue in the second quarter.

The bank declined to comment on its expectation for technology spending this year, or what it’s invested in the mobile app specifically. A spokesperson said Fifth Third has 735 technology employees in Cincinnati, and about 300 team members across technology, product, design and other areas of the company worked on development of the mobile app.

Behind the scenes, Fifth Third has sought to be intentional with its approach to digital, with the way it’s practically integrated into the organizational structure.

The approach the bank has taken, and one the reasons Hoffman has a “somewhat odd mandate”: If digital lives off to the side, and the mobile app is disconnected from product and run by IT as a piece of technology not powered by research, “you risk doing work for its own sake,” he said.

And the collaboration among product, technology and design is reflected in physical co-location and culture at the bank, Hoffman said. Teams are structured by customer jobs to be done – like getting into the app or getting paid – rather than by product.

“When you organize that way and then you embed customer research and co-development with the customers at every step, you focus on the things that matter more to customers, and you ensure a higher degree of relevance and salience,” he said.

That mindset continues to drive further enhancements. For one, Fifth Third is working on driving “more smarts” into Jeanie, the bank’s virtual banking assistant; the bank has sought to hone its ability to understand what a customer wants.

“We are certainly imagining a world in which you can achieve much of everyday banking in sort of native language interaction with Jeanie, just as you do today through screens and taps in a traditional mobile interface,” Hoffman said.

Fifth Third is also undertaking improvements to SmartShield and its customers’ Zelle experience, including helping clients manage fraud risk.

Hoffman said he expects material releases or substantial developments in the next six months in each of those areas.

The bank has focused its initial deployments of artificial intelligence in a couple of key places – “we work very hard to not use AI for its own sake,” Hoffman said – with Jeanie being one of those. “Hyper-customized” product and service recommendations, as well as identity and fraud protection, are the other areas, he noted.

Article top image credit: Permission granted by Fifth Third Bank

Making sense of the ‘crazy quilt’ of financial regulators

Federal banking agency job cuts and a deregulatory push have again stoked conversations around consolidation. Merging agency functions could make sense, but here’s why it’s unlikely to happen.

By: Caitlin Mullen• Published July 1, 2025

As the U.S. bank regulatory system has grown throughout history, so have calls to simplify it.

Bank of America CEO Brian Moynihan this year lamented “the spaghetti chart of overlap” among bank regulators and reiterated suggestions from big-bank executives that it’s time to “start with a fresh sheet of paper.”

The bank regulatory system is a fragmented, complex web that involves a host of national and state agencies focused on lenders operating safely and soundly. Despite periodic efforts to consolidate functions, the general framework is likely here to stay, many observers said.

Each federal agency supervises banks under different charter types. National banks are supervised by the Office of the Comptroller of the Currency; state member banks are supervised by the Federal Reserve and state bank regulators; and state non-member banks are supervised by the Federal Deposit Insurance Corp. and state regulators. The Fed’s purview also extends to bank holding companies and foreign bank offices in the U.S., among other entities.

Additionally, the FDIC manages deposit insurance and failed bank resolutions, while the Fed handles monetary policy and serves as the lender of last resort.

While the framework offers banks choice and fosters competition among regulators, it’s a system that’s tough to figure out if you’re new to it. “If you were to start it from scratch, you wouldn’t want it this way,” said Konrad Alt, co-founder of financial services advisory and investing firm Klaros Group.

How did America’s banking system get here? Federal banking agencies were created in response to crises, where Congress has perceived gaps in oversight. Many agree consolidation is a good idea, even if they differ on the details.

“But the forces of the status quo are strong,” Alt said.

The genesis of why there are so many bank regulators is essentially “trying to understand how the government is managing financial risk,” said Sean Vanatta, a senior lecturer in financial history and policy at the University of Glasgow and co-author of “Private Finance, Public Power: A History of Bank Supervision in America.”

The federal prudential regulators are:

The OCC, a bureau of the Treasury Department, was created in 1863, with the National Currency Act. That law was “a response to the mishmash of local banks, local money, and conflicting regulatory standards that prevailed before the Civil War,” according to the OCC. It created a new type of federally chartered bank that would float bond offerings to finance the Civil War. But the chartering focus – creating banks and enforcing the rules under which banks operate – didn’t provide an effective means of combating crisis. The comptroller didn’t have a balance sheet, so it couldn’t provide liquidity to financial markets, and it was difficult to oversee the thousands of banks that were created across the U.S.

The Fed was established in 1913 by the Federal Reserve Act, creating a network of reserve banks in large cities and a board of governors in Washington, D.C. The idea was the Fed would focus on central banking and liquidity as a way to manage financial risk distinct from what the OCC or state banking agencies were doing. But during the Great Depression, “it becomes clear that together those two models aren’t really working effectively to prevent crisis,” Vanatta said.

The FDIC was created through the Banking Act of 1933, after thousands of banks failed in the 1920s and early 1930s. President Franklin D. Roosevelt sought to reassure depositors their money would be safe in banks, teeing up the national system of deposit insurance.

While the three regulators were initially seen as alternatives, the U.S. took the position after the Great Depression that central banking, deposit insurance and chartering institutions – whether the OCC or the states – were all needed.

“It’s that kind of repeated process of adopting a risk management framework that’s sort of narrow, and that framework on its own not working effectively enough to prevent financial crisis,” resulting in the current system, Vanatta said.

Predating all of this is state supervision of banks, going back to the early 19th century. Today, it’s a disparate group, since some state bank regulators oversee a large number of banks, while others provide oversight for far fewer banks.

“It is a crazy quilt design that is the product of historical accident, and we’re probably going to stick with it,” said Patricia McCoy, a law professor at Boston College and a former assistant director at the Consumer Financial Protection Bureau.

The CFPB is another financial regulator, though focused on the consequences to consumers rather than the functions of banking itself. Additionally, there’s the Securities and Exchange Commission to consider. And the Commodity Futures Trading Commission, the Federal Trade Commission, the Financial Crimes Enforcement Network and the Federal Financial Institutions Examination Council. The National Credit Union Administration regulates, charters and supervises federal credit unions.

There’s overlap across the system, but that’s been established by Congress, not the agencies themselves. For banks, the compliance cost of that regulatory overlap can be enormous. BofA’s Moynihan noted this year “there’s 100-plus regulators in our building every day.”

Creative via Getty Images

Why hasn’t much changed?

There’s always been pressure around bank regulatory consolidation. Such efforts tend to recur every 15 to 20 years going back to the 1950s, Alt said.

The creation of the Fed, for example, prompted questions about the need to keep the OCC, in part because that move revoked the currency focus for the comptroller. And state versus federal chartering creates different incentives to loosen or strengthen rules as the states and federal government compete over bank charters.

But consolidation efforts, thus far, have fallen short. Alt can testify to that: While a staffer on the Senate Banking Committee, he spent two years working on legislation to consolidate regulators; it garnered bipartisan support in the House and Senate in the early 1990s, but ultimately wasn’t passed.

The bank regulatory system “works adequately, and therefore the case for reform isn’t all that compelling,” Alt said. “It’s strong, logical, but it’s not urgent.”

Pursuing formal consolidation would require congressional action, and therein lies a challenge to proposed reforms.

“Even members of Congress who agree that federal banking legislation should be streamlined may not be able to agree on how to do that,” said Karen Solomon, senior of counsel at law firm Covington & Burling and former OCC official.

Some 21st-century considerations around consolidation involve isolating bank supervision within the OCC, retaining central banking functions at the Federal Reserve, and maintaining the FDIC’s role as deposit insurer.

The need for both state and national chartering is less obvious to some. Others see an opportunity to consolidate all state-chartered banks under a single federal regulator.

An exception among past failed attempts: The Office of Thrift Supervision, which supervised savings and loans institutions, was abolished as part of the Dodd-Frank Act. Congress rolled some of OTS’ functions into the OCC and others into the CFPB.

Merging functions, however, comes with its own considerations, including innovation versus risk and independence from politics.

There are benefits to the current system, including diversity of perspectives and objectives, observers said. “There’s value in having focused risk managers who adopt these different frameworks,” Vanatta said.

The banking system largely isn’t interested in a single regulator with concentrated power. Competition among various bank regulators is healthy and keeps the system on its toes, said Michael Hsu, former acting head of the OCC.

It’s an issue that can pit large banks against small: Bigger banks tend to be annoyed by the plethora of regulators, but smaller banks like the choice, Hsu said. “It does feel like Hamilton versus Jefferson,” he said during a June Brookings event. “That tension’s always been there.”

And the resources required to stay on top of such a large and complicated banking system demand a sizable apparatus.

There’s a comfort factor, too: Consolidation attempts fail “because individual institutions want things the way they are,” said Karen Petrou, managing partner at Federal Financial Analytics. There are, to some degree, captive regulators “everybody’s quite comfortable with,” and arbitrage opportunities between national and state charters that banks don’t want to lose, she added.

Consolidation also presents the possibility that surviving regulators have to split their focus. If FDIC banks were moved under OCC supervision, for example, “if you’re the OCC, where are you going to focus your attention?” said Matthew Bisanz, a partner at the law firm Mayer Brown focused on financial regulation.

“Are you going to focus it on these 4,000 little banks and their unique needs of elder abuse, and branches, and agricultural lending?” Bisanz said. “Or are you going to focus it on the eight money center banks, the failure of any one could bring down the country?”

The Marriner S. Eccles Building, home of the Federal Reserve Board

Douglas Rissing via Getty Images

What’s different in the current moment?

With sizable staff cuts at banking agencies – including apparent attempts to all but shut down the CFPB – “it’s clearly the intent of the Trump administration to merge agencies,” said Peter Dugas, executive director at consulting firm Capco.

The Trump administration, amid broader efforts to shrink the size of the federal government, has moved “quickly and aggressively” to modify organizational and staffing models for the agencies, Dugas said. That development points to more unknowns.

Given the administration’s propensity to attempt major actions by executive order, it’s possible the White House may try to realize consolidation that way. Most likely, observers said, is that the Trump administration pursues cost efficiencies and reduces regulatory burdens to garner similar results to what restructuring could produce.

Having Treasury Secretary Scott Bessent act as a sort of “conductor” over the federal banking agencies appears to be another element to the Trump administration’s plans to achieve regulatory reform.

“There is going to be a good deal more coordination amongst the agencies acting as the Treasury Department and thus the White House would like them to act when it comes, at the very least, to regulation and perhaps also supervision,” and that’s unique, Petrou said.

Even if consolidation “seems like an impossible dream” or a massive legislative package not worth pursuing, greater efficiency within the system is needed, said Donald Kohn, who served as vice chair of the Fed from 2006 to 2010.

“There’s got to be a way of moving faster, coordinating better, overcoming some of the objection, so that if a risk is identified, it doesn’t take three years to identify how to build the resilience against that risk,” Kohn said during the Brookings event. “We need to make it more effective and efficient if we’re going to keep all those agencies.”

Consolidation can also be reframed as a chance to capitalize on various agencies’ core strengths to enhance supervision, said Sarah Bloom Raskin, a law professor at Duke University and Biden administration nominee to be the Fed’s vice chair for supervision, during the Brookings event.

Discussions around the bank regulator framework are likely to continue, and that’s a good thing, observers said.

“It is a mistake to just assume that they’re working and that they’re working effectively,” Vanatta said. “[But] it’s better to ask those questions and make decisions – informed decisions – rather than just coming in with a chainsaw, carving things up and hoping for the best.”

Article top image credit: Creative via Getty Images